A card terminal abroad may show your home currency and ask you to confirm a payment amount that looks familiar. That moment — when the screen switches from local currency to your own — is usually a dynamic currency conversion offer. It can look convenient. It deserves a closer look before you tap or sign.

Dynamic currency conversion, often shortened to DCC, is a service offered by some merchants, payment terminals, booking platforms, or ATMs. It converts a foreign transaction into the cardholder’s home currency before the payment is completed — at a rate set by the merchant, ATM operator, or their payment processor, not by your card network in the standard way.

This is the next step after understanding foreign transaction fees abroad. A card with no foreign transaction fee can still produce a higher final cost if you accept an unfavorable currency conversion offer at the terminal or ATM.

Last updated: May 2026. Currency conversion rules, card network requirements, bank fees, exchange rates, and ATM or merchant practices can change. Always review the payment screen carefully and confirm your own card terms before relying on any currency choice abroad.

How this guide was prepared: This guide focuses on practical payment checks travelers can use when a card terminal, ATM, or online checkout offers a choice between local currency and home currency. It uses official card network guidance, consumer finance principles, and payment transparency rules as reference points. Dynamic currency conversion terms can vary by merchant, ATM operator, payment processor, card network, card issuer, country, and transaction type.

1. What Is Dynamic Currency Conversion?

Dynamic currency conversion is a point-of-sale or ATM service that offers to convert a transaction into the cardholder’s home currency before the payment is completed. The conversion rate and any markup are set by the merchant, ATM operator, or their payment processor — not by your card network in the standard way.

You may encounter it when:

- Paying by card at a restaurant, shop, or hotel abroad

- Checking out at a hotel front desk

- Buying tickets, passes, or activity bookings overseas

- Withdrawing cash from an ATM abroad

- Paying on a foreign travel or booking website

- Using a card terminal that recognizes your card’s home currency

The screen may ask something like:

- “Pay in USD or EUR?”

- “Continue with conversion?”

- “Accept guaranteed exchange rate?”

- “Debit in your home currency?”

- “Pay in your card currency?”

The exact wording varies by terminal, merchant, and country. The key pattern is the same: the merchant, ATM, or payment provider is offering to convert the transaction before it reaches your card issuer.

💡 Practical rule: If a terminal or ATM offers to convert the transaction into your home currency, pause before accepting. You are likely looking at a dynamic currency conversion offer. Check the rate and markup before deciding.

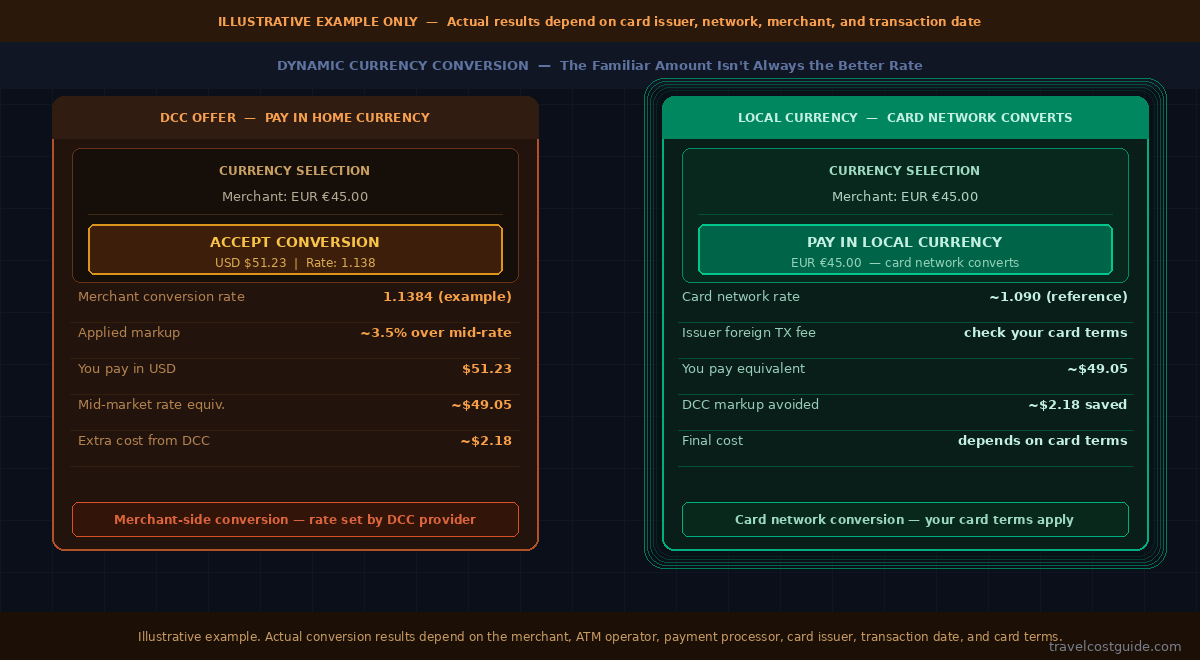

2. Why DCC Can Cost More

DCC can cost more because the conversion rate is set at the point of sale by the merchant, ATM operator, or payment processor offering the conversion — not by your card network. That rate may include a markup or additional fee on top of the underlying exchange rate.

Visa explains that when DCC is offered, the screen and receipt should clearly show the transaction amount in both the local currency and the cardholder’s currency, the exchange rate used, and any additional fees or markup. The cardholder should also be able to accept or decline the conversion. If those details are missing or the cardholder feels pressured toward a particular option, Visa recommends declining the currency conversion offer and reporting the issue to the card issuer.

The important point for travelers is this: seeing the amount in your home currency does not mean the conversion is cheaper. It means the amount is easier to recognize. The rate applied may still be less favorable than your card network’s standard conversion.

| Choice | What It Means | Who Handles Conversion? |

|---|---|---|

| Pay in local currency | Transaction stays in the merchant’s currency | Your card network or issuer typically handles conversion at settlement |

| Pay in home currency (DCC) | Transaction is converted before you approve | Merchant, ATM, or DCC provider handles conversion |

In many cases, choosing the local currency is the safer habit because it avoids merchant-side conversion. However, the final cost still depends on your card terms, any foreign transaction fee, the applicable exchange rate, and how the transaction is ultimately processed.

3. DCC Is Not the Same as a Foreign Transaction Fee

DCC and foreign transaction fees are related, but they are separate costs that come from different sources.

- Dynamic currency conversion: A merchant, ATM, or payment processor converts the amount into your home currency before you approve the transaction. The rate and any markup are set by the provider, not your card network.

- Foreign transaction fee: A fee your card issuer may charge when a transaction involves a foreign merchant, foreign currency, or cross-border processing — separate from what the merchant does at the point of sale.

These costs can overlap. A traveler might accept DCC and still be charged a foreign transaction fee by their card issuer, depending on the card agreement and how the transaction is classified. A traveler might also use a card with no foreign transaction fee and still pay more overall if the DCC exchange rate is unfavorable.

This is why “no foreign transaction fee” does not automatically mean no extra payment cost abroad. It solves one problem — not every currency conversion problem.

💡 Practical rule: DCC is about who converts the currency — the merchant or ATM, before you approve. A foreign transaction fee is what your card issuer may charge under your card terms. Both can affect your final cost. Check them separately.

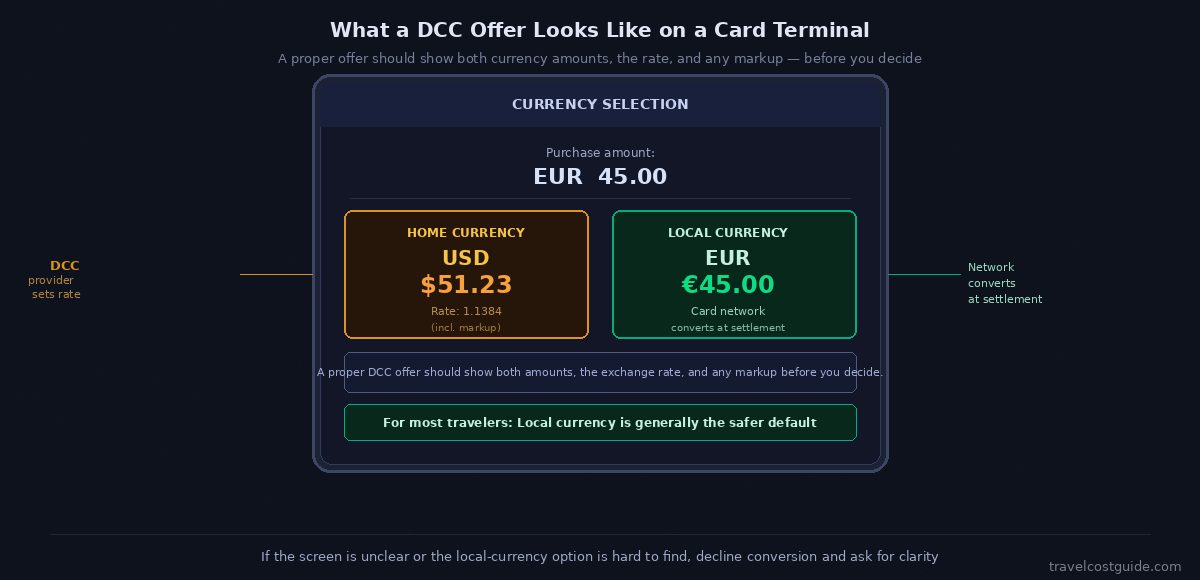

4. What the Terminal Screen May Look Like

DCC screens are not always clearly labeled. Some terminals present the home-currency amount more prominently, use reassuring phrases, or make the local-currency option less obvious.

Watch for these patterns:

- Your home currency appears on a terminal in a foreign country

- The screen asks whether you want conversion or offers to convert for you

- The terminal displays a “guaranteed rate” or “no surprises” message

- The local-currency amount or the option to decline is smaller or harder to find

- The screen asks you to “accept” an exchange rate without showing the markup

- An ATM shows your home currency amount before processing withdrawal

A proper DCC offer should allow you to see the local-currency amount, the home-currency amount, the exchange rate, and any added fee or markup before you decide. If that information is missing, unclear, or the staff member selects an option without asking you, the safer response is usually to decline the conversion and proceed in the local currency when possible.

If you are unsure which option you selected, keep the receipt and compare it with your card statement later to understand the final converted amount.

5. Local Currency vs. Home Currency: The Safer Default for Most Travelers

When paying abroad, choosing the local currency is the safer default for most travelers in most situations.

Local currency means the currency normally used by the merchant, hotel, ATM, or service in the country you are visiting — for example:

- EUR in countries using the euro (eurozone)

- JPY in Japan

- KRW in South Korea

- THB in Thailand

- GBP in the United Kingdom

- CAD in Canada

Choosing local currency generally avoids the merchant or ATM operator’s conversion rate. Your card network or issuer then processes the conversion under your card’s own terms.

However, this is not the same as saying every local-currency payment is free or always cheaper. Your card may still charge a foreign transaction fee. The exchange rate applied by your card network can also vary by processing date. Local currency removes one cost layer — merchant-side conversion — but the other layers still apply.

💡 Practical rule: Local currency is usually the cleaner choice because it removes the merchant or ATM operator’s conversion from the equation. You still need to know your card’s own foreign transaction fee and exchange-rate method.

6. DCC at ATMs Needs Its Own Check

Dynamic currency conversion can also appear when withdrawing cash from an ATM abroad. The ATM may ask whether you want to:

- Accept the ATM’s conversion rate

- Continue with conversion

- Withdraw in your home currency

- Accept a “guaranteed exchange rate”

- Proceed without conversion

ATM DCC screens can include multiple confirmation steps that resemble warnings but may be structured in a way that moves toward accepting conversion. The ATM operator may also charge its own separate withdrawal fee on top of any currency conversion.

For many travelers, the safer habit at ATMs is the same as at terminals: decline the ATM’s currency conversion and withdraw in the local currency. But you should still check your bank’s international ATM fee, the ATM operator fee, and your card’s foreign transaction fee separately — these apply regardless of which currency you choose.

Mastercard notes that its currency conversion rates may not apply if a transaction is converted by the merchant or ATM operator rather than by the card network. This typically happens when the cardholder accepts the home-currency option at the point of sale or ATM screen.

ATM fees — including operator charges, bank fees, and withdrawal limits — are a separate cost layer covered in the next guide in this series.

7. Online DCC and Travel Booking Screens

DCC is not limited to physical terminals. It can also appear in online travel bookings when a platform offers to display or charge prices in your home currency.

You might see a currency choice when booking hotels, flights, trains, activities, car rentals, local transport passes, or event tickets on foreign platforms. Display currency and payment currency are not always the same thing — a site may show prices in your home currency for convenience while actually charging in local currency, or vice versa.

Before approving any online payment, check:

- The currency you are actually being charged in on the final checkout page

- Whether the platform is applying its own conversion or a conversion fee

- Any service fee or markup shown at checkout

- The merchant’s billing country, which may affect whether your card charges a foreign transaction fee

A price display in your home currency helps with planning and comparison, but it should not be treated as confirmation that the payment will be cheaper than paying in the local currency.

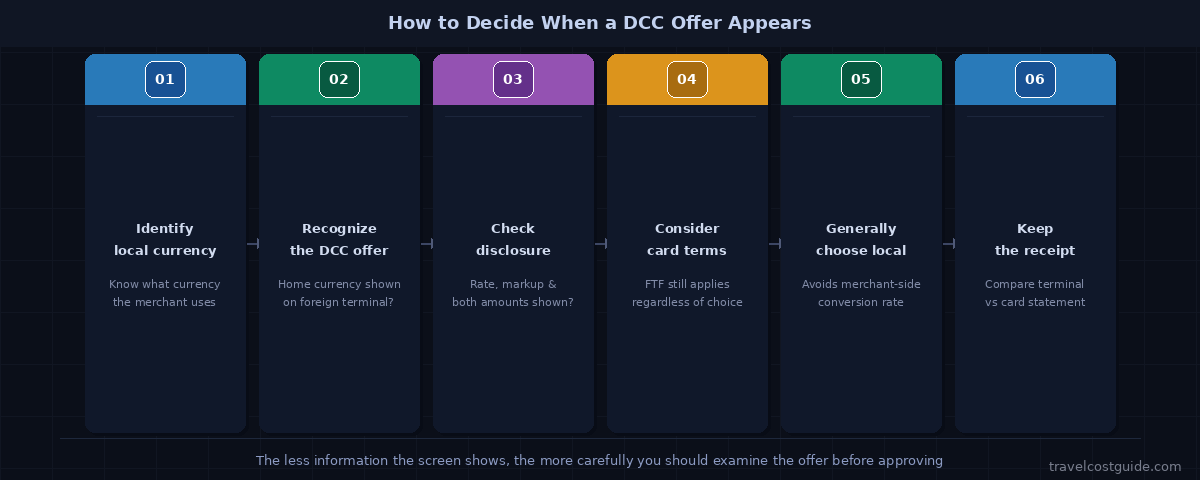

8. How to Decide When DCC Appears

When a terminal, ATM, or checkout screen offers dynamic currency conversion, a simple decision process can help:

- Identify the local currency. Know what currency the merchant, hotel, ATM, or website normally charges in.

- Recognize the DCC offer. If your home currency appears on a foreign terminal or ATM, you are likely being offered DCC.

- Check what is disclosed. A proper offer should show the local-currency amount, home-currency amount, exchange rate, and any markup or fee before you decide.

- Compare with your card terms. Your card’s own foreign transaction fee and conversion method still apply regardless of which currency you choose.

- Choose local currency in most cases. This removes the merchant or ATM operator’s conversion rate from the transaction.

- Keep the receipt. Compare the terminal amount with your final card statement to understand what was actually charged.

If the screen does not clearly show the exchange rate, markup, or local-currency amount, that is a reason to be cautious. The less information the screen shows, the more carefully you should examine the offer before approving.

Where to Verify DCC Information Before Paying Abroad

Because DCC depends on the payment screen and the provider offering conversion, preparation before travel is limited — but useful.

- Visa DCC guidance: Visa’s official resources explain that a DCC offer should disclose both currency amounts, the exchange rate, and any additional fees or markup, and that cardholders have the right to decline. Visa’s dynamic currency conversion guidance page explains what information must be disclosed and how cardholders can accept or decline the offer.

- Mastercard currency converter: The Mastercard currency converter provides reference rate estimates. Mastercard notes that its rates may not apply when the merchant or ATM operator performs the conversion directly.

- Your card’s fee table and cardholder agreement: Check whether your card charges a foreign transaction fee even when you decline DCC, and how your issuer handles cross-border transactions.

- ATM screen before withdrawal: Read all screens carefully before confirming. Look for the local-currency option and any conversion offer before approving.

- Final checkout screen for online bookings: Confirm the actual payment currency before completing the transaction.

- Receipt and card statement: Compare the approved terminal amount with the final charged amount to understand what was applied.

- EU payment services information: In the European Economic Area, payment service regulations require, where applicable, that currency conversion fees be disclosed as a percentage markup over the European Central Bank reference rate before a transaction is approved. If traveling in the EEA, merchants and ATMs should disclose this information at the point of sale — though actual compliance and disclosure practices can vary.

Official tools and card network resources can help you understand how conversion works, but they do not guarantee your final statement amount. Your actual cost depends on your card terms, the transaction date, the payment processor, and whether merchant-side or ATM-side conversion was applied.

Frequently Asked Questions

Is dynamic currency conversion always bad?

Not always — but DCC can be more expensive than paying in local currency, because the rate and any markup are set by the merchant or ATM operator rather than your card network. The safer habit for most travelers in most situations is to decline DCC and pay in local currency. However, the final outcome depends on the rate offered, your card terms, and the transaction details.

Does a no-foreign-transaction-fee card protect me from DCC?

No. A no-foreign-transaction-fee card removes your issuer’s foreign transaction fee, but it does not prevent a merchant or ATM from offering DCC. If you accept DCC, the conversion happens before the transaction reaches your card issuer — your card’s fee terms apply to what arrives at the issuer, not what was converted at the point of sale.

Can I still be charged a foreign transaction fee if I decline DCC?

Yes, depending on your card terms. Declining DCC means the transaction stays in local currency, which is generally cleaner. But your card issuer may still apply a foreign transaction fee if your card charges one for cross-border or foreign-merchant transactions.

What should I choose at a card terminal abroad?

In most cases, choosing the local currency is the safer default. It removes the merchant’s conversion rate from the transaction. You should also know your card’s own foreign transaction fee and exchange-rate terms, since those still apply.

What should I choose at an ATM abroad?

If the ATM offers to convert the withdrawal into your home currency, the safer habit for most travelers is to decline and withdraw in local currency. Also check the ATM operator fee, your bank’s international ATM fee, and your card’s foreign transaction fee — these apply regardless of the currency choice.

Is display currency the same as payment currency?

No. A travel website may display prices in your home currency for convenience, but the actual payment currency at checkout may be different. Always check the final checkout page before approving. The displayed amount and the charged amount can differ.

What if I already accepted DCC by mistake?

If you accepted DCC and later notice the converted amount on your card statement looks higher than expected, you can compare it with the local-currency amount on your receipt and the card network’s reference rate for that date. If you believe the conversion was applied without proper disclosure or without your consent, you can raise the issue with your card issuer. Whether a dispute or refund is possible depends on your card agreement, the card network’s rules, and the circumstances of the transaction.

Dynamic Currency Conversion Checklist Before You Pay

Before accepting any currency conversion offer abroad, run through this:

Terminal or ATM Screen

- Is the terminal showing my home currency in a foreign country?

- Can I clearly see the local-currency amount?

- Can I clearly see the exchange rate being applied?

- Can I see any added fee or markup disclosed?

Currency Choice

- Do I know the local currency of this country?

- Am I choosing local currency unless I have a clear reason to accept conversion?

- Am I aware that “guaranteed rate” language does not mean a better rate?

Card Terms

- Does my card charge a foreign transaction fee even if I decline DCC?

- Does my card issuer use card network conversion rates or another method?

- Do I understand that DCC and foreign transaction fees are separate costs?

After Payment

- Did I keep the receipt?

- Have I checked the final card statement amount?

- Did the charged amount match what I expected?

The Bottom Line

Dynamic currency conversion is a currency conversion choice — not automatically fraud, but often a more expensive option than letting your card network handle the conversion. The home-currency amount may look familiar and convenient on the terminal screen while the applied rate may include a markup that raises the final cost.

For most travelers in most situations, the safer habit is straightforward: when given a currency choice abroad, choose the local currency and let your card network or issuer handle the conversion under your card’s own terms. Then review your statement to understand what was actually charged.

DCC is one of the more avoidable travel payment costs because the choice usually appears on screen before you approve the transaction. Recognizing the offer — before you tap, sign, or press confirm — is the main skill required.

DCC and foreign transaction fees work together as two separate cost layers on every international card payment. Understanding both — covered in the foreign transaction fees guide and this guide — gives you a complete picture of what determines the final amount on your statement.

The next payment layer is cash access: ATM operator fees, bank fees, and withdrawal screens that can present their own conversion choices. ATM Fees Abroad: What Travelers Should Check Before Withdrawing Cash →