A card statement after an international trip can show higher amounts than the prices paid at the point of purchase. The difference may come from currency conversion, a foreign transaction fee applied by the card issuer, a merchant-side conversion accepted at checkout, or a combination of these. None of these charges are always visible at the moment of payment.

The goal is not to make every international payment free. Some fees depend on your card, bank, country, merchant, payment network, and transaction currency. The goal is to understand where the fees appear and how to avoid unnecessary charges when better options are available.

This is the next step after checking hotel hidden fees. Once you understand the real cost of flights and accommodation, the next layer is how you pay for them — and what that payment actually costs.

Last updated: May 2026. Card fees, exchange rates, payment network rules, and bank policies can change. Always confirm current terms with your card issuer, bank, payment network, or booking platform before relying on a specific payment method abroad.

How this guide was prepared: This guide focuses on practical payment checks travelers can make before and during an international trip. It uses official consumer finance resources, card network currency conversion tools, and card-fee disclosure principles as reference points. Foreign transaction fees vary by card issuer, bank, country, card type, payment network, transaction currency, and merchant — always verify the terms of your own card before traveling.

1. What Is a Foreign Transaction Fee?

A foreign transaction fee is a charge that may apply when a card transaction involves a foreign country, foreign merchant, foreign currency, or cross-border processing. The fee may be charged by the card issuer or reflected through the issuer’s foreign transaction pricing structure. The exact rule depends on your cardholder agreement.

For travelers, this can apply in more situations than expected:

- Paying at a restaurant, shop, or hotel abroad

- Booking a hotel through an overseas merchant’s website — before you leave

- Buying train tickets or tour packages from a foreign operator online

- Withdrawing cash from an ATM abroad using a debit or credit card

- Making any purchase where the merchant or processing location is outside your home country

- Paying in your home currency while physically abroad (which may still trigger foreign transaction terms)

Some cards charge no foreign transaction fee at all. Others charge a percentage — often in the range of 1–3% — but the exact rate depends on your card issuer and cardholder agreement. Do not assume a card is travel-friendly simply because it works internationally. Check whether it charges foreign transaction fees before using it as your primary travel card.

💡 Practical rule: Check your card’s rates and fees table specifically for “foreign transaction fee,” “international transaction fee,” “currency conversion fee,” or “cross-border fee” before traveling. These terms can vary by issuer.

2. Foreign Transaction Fees, Exchange Rates, and Dynamic Currency Conversion Are Three Different Things

A common mistake is treating these three as the same thing. They are not — and understanding the difference matters for how you manage costs abroad.

- Exchange rate: The rate used to convert one currency into another. Card networks such as Visa and Mastercard publish reference rates, but the rate applied to your transaction depends on when it is processed and whether your issuer applies its own conversion method.

- Foreign transaction fee: A fee charged under your card’s or issuer’s foreign transaction terms. This is separate from the exchange rate itself.

- Dynamic currency conversion (DCC): A merchant or ATM-side offer to convert the purchase amount into your home currency at checkout or withdrawal. The conversion rate used by the merchant or ATM may differ from the rate your card network would apply.

These three can overlap, but they operate independently. A card can have no foreign transaction fee and still produce a higher final cost if the cardholder accepts an unfavorable dynamic currency conversion at the point of sale. A card can use a reasonable exchange rate but still charge a separate foreign transaction fee on top. Understanding which cost is coming from where is the first step to managing them.

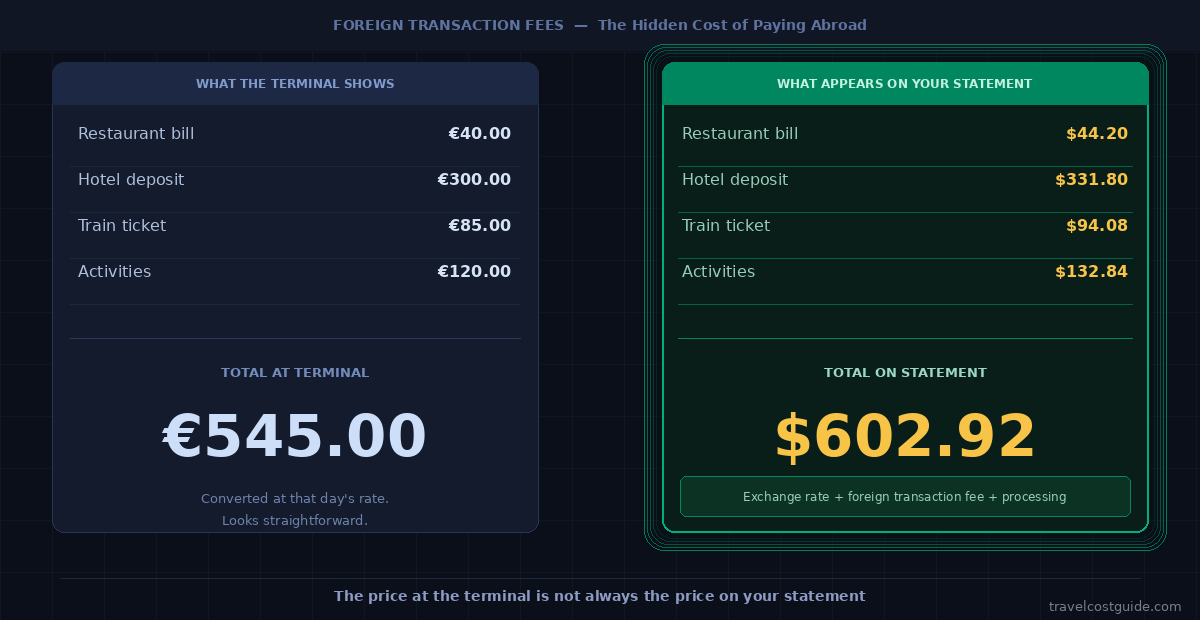

3. How Foreign Transaction Fees Can Add Up: An Illustrative Example

The numbers below are only an illustrative example using a 3% foreign transaction fee. Your actual fee depends on your card issuer, transaction currency, payment network, and card agreement. Not all cards charge this rate, and some charge no foreign transaction fee at all.

| Travel Purchase | Amount | 3% Fee (example only) |

|---|---|---|

| Hotel payment | $800 | $24.00 |

| Restaurants | $350 | $10.50 |

| Transportation | $180 | $5.40 |

| Activities | $250 | $7.50 |

| Shopping | $300 | $9.00 |

| Total | $1,880 | $56.40 |

In this illustrative scenario, the fee does not destroy the trip budget. But it is a real cost — and one that is easy to miss because it appears after the purchase, not at the terminal. Travelers who make frequent international trips, pay for family expenses, or use the same card for every purchase without checking its fee terms can accumulate meaningful charges over time.

4. When a Foreign Transaction Fee Can Apply — Including Before You Leave

Foreign transaction fees are not limited to purchases made while you are physically abroad. A pre-trip online booking can still be treated as a foreign transaction depending on the merchant’s location, the transaction currency, the processing channel, and your card’s terms.

Common situations where a foreign transaction fee may apply:

- Paying abroad in local currency: A normal card purchase in another country may trigger the fee if your card charges one.

- Paying abroad in your home currency: Accepting a merchant’s currency conversion does not automatically prevent a foreign transaction fee — the merchant may still be classified as a foreign merchant under your card terms.

- Online bookings before travel: Foreign airlines, international rail operators, hotel websites, vacation rental platforms, tour operators, local transport apps, and event ticketing sites may all be processed as foreign merchants even when booked from home.

- Debit card purchases abroad: Debit cards may carry their own foreign transaction fees, separate from any ATM-related charges.

- Prepaid travel cards: These products can include reload fees, ATM withdrawal fees, inactivity fees, currency conversion fees, card issuance fees, and balance refund fees. Check the product’s full fee schedule before relying on it as your primary travel payment method.

Card acceptance and fee structures also vary by destination. In some countries and regions, contactless card payments are standard. In others, cash remains common and ATM access becomes more important. The right payment setup depends on where you are going as well as which card you carry.

💡 Practical rule: Check your card’s fee table before making any international booking — online or in person. The fee may apply whether or not you are physically present in the foreign country at the time of the transaction.

5. How to Reduce Foreign Transaction Fees

The most direct way to reduce or avoid foreign transaction fees is to use a card whose terms do not charge them. However, a card with no foreign transaction fee is not automatically the best choice for every traveler or every trip.

Before choosing a card for international travel, check:

- Does the card charge a foreign transaction fee?

- Does the fee apply to purchases only, or also to cash advances?

- Does the fee apply to online foreign merchants?

- Does the card issuer use the card network exchange rate or apply its own conversion method?

- Does the card carry an annual fee that may offset any fee savings?

- Does the card work reliably and widely at your destination?

- What are the card’s ATM access rules and cash advance terms?

- Does the card include meaningful fraud and security protections for international use?

- Do you have at least one backup card in case of acceptance issues or card blocks?

A no-foreign-transaction-fee card can reduce one specific cost. It does not automatically solve exchange rate differences, ATM operator fees, dynamic currency conversion choices, cash advance charges, or destination-specific acceptance issues. Evaluate the full picture before deciding which card to use as your primary travel payment method.

💡 Practical rule: Solving the foreign transaction fee is one step. Checking all the other costs that can appear around an international payment is the complete picture.

6. Paying in Local Currency vs. Your Home Currency

When paying by card abroad, a terminal or ATM may ask whether you want to pay in the local currency or your home currency. This is typically an offer of dynamic currency conversion.

Choosing your home currency may feel more familiar because the amount is displayed in a recognizable number. However, the conversion rate offered by the merchant or ATM at that moment may be less favorable than the rate your card network or issuer would otherwise apply.

In many cases, choosing the local currency is the safer habit because it avoids a merchant-side conversion rate. However, the final cost still depends on your card’s own conversion method, any applicable foreign transaction fee, and how the transaction is ultimately processed.

For most travelers, a reasonable general approach is:

- Generally choose the local currency at card terminals when given a choice

- Decline merchant-offered currency conversion when possible

- Review your card statement after the trip to see the actual converted amounts

- Use Visa or Mastercard’s online currency tools as reference estimates — not as guarantees of your final charged amount

Dynamic currency conversion involves its own considerations and variations. The next guide explains how DCC works and how to identify it at payment terminals.

7. Debit Cards, ATM Withdrawals, and Cash Advances

Using a debit card or withdrawing cash abroad involves a separate set of potential costs from standard card purchases. These costs can include:

- Your bank’s foreign transaction fee on the debit card purchase or withdrawal

- Your bank’s international ATM fee

- The ATM operator’s own fee, charged separately

- A dynamic currency conversion offer at the ATM (which can be declined)

- Withdrawal limits that may affect how much cash you can access per transaction or per day

A card that works well for restaurant purchases may not be the most cost-effective option for ATM withdrawals. A debit card with low ATM fees may still charge a foreign transaction fee on withdrawals. These fee categories can stack, so it is worth checking them individually before travel.

Credit card cash advances are a separate situation. Using a credit card to withdraw cash at an ATM is different from a normal card purchase and may involve cash advance fees, a different interest rate that begins immediately, and separate limits. Check your credit card’s terms before using it to access cash abroad.

ATM fees and strategies for reducing cash-access costs deserve their own review — covered in a dedicated guide in this series.

💡 Practical rule: Check your bank’s international ATM rules and your debit card’s foreign transaction fee separately before travel. Also identify at least one backup method for accessing cash in case of ATM availability issues.

8. Where to Verify Foreign Transaction Fees Before Travel

Because foreign transaction fees depend on your specific card and issuer, general travel advice cannot replace your own card’s fee disclosure. Verify from primary sources before relying on any payment method abroad.

- Your card’s rates and fees table: Look specifically for “foreign transaction fee,” “international transaction fee,” “currency conversion fee,” or “cross-border fee.” This document is usually available on your issuer’s website or in your account portal.

- Your cardholder agreement: Check whether fees apply to purchases, cash advances, online foreign merchants, or foreign-currency transactions specifically.

- Your bank’s international ATM and debit card fee page: Confirm whether your bank charges a fee for international ATM use, and whether ATM operator fees apply on top.

- Visa’s exchange rate calculator: Available at the Visa currency converter. Use it as a reference estimate for Visa card conversion — your issuer may apply additional fees or use a slightly different rate depending on processing date and card terms.

- Mastercard’s currency converter: Available at the Mastercard currency converter. Use it as a reference estimate — if a merchant or ATM offers its own currency conversion, the card network rate may not apply to that transaction.

- CFPB foreign transaction fee guidance: The Consumer Financial Protection Bureau’s explanation of foreign transaction fees provides a plain-language overview of how these fees work and where they appear.

- The final checkout or ATM screen: Confirm the transaction currency, total amount, and whether a currency conversion is being offered before approving the payment.

Official tools can help estimate conversion, but they do not replace your issuer’s fee disclosure. Your final cost depends on your card’s terms and how the transaction is processed.

Frequently Asked Questions

Is a foreign transaction fee always 3%?

No. Some cards charge no foreign transaction fee, some charge a different percentage, and some card products use different fee structures. The rate depends on your card issuer and cardholder agreement. Check your own card’s rates and fees table before traveling — do not assume a standard industry rate applies.

Can I still get charged a foreign transaction fee if I pay in my home currency abroad?

Yes, depending on your card agreement and how the transaction is processed. Paying in your home currency at a foreign merchant does not automatically prevent a foreign transaction fee from applying — the transaction may still be classified as a foreign or cross-border transaction under your card’s terms. It may also result in dynamic currency conversion being applied.

Are foreign transaction fees the same as dynamic currency conversion?

No. A foreign transaction fee is typically related to your card issuer’s terms for cross-border transactions. Dynamic currency conversion is a merchant or ATM-side currency conversion offer made at checkout or withdrawal. Both can affect the total amount you pay, but they come from different sources and apply under different conditions.

Are debit cards cheaper than credit cards for international payments?

Not automatically. Debit cards may carry ATM fees, foreign transaction fees, bank fees, and DCC costs. Credit cards may reduce some ATM-related costs for purchases, but can be significantly more expensive for cash advances. The right choice depends on your specific card terms, the type of payment being made, and the destination. Compare your actual card and bank terms before deciding.

Should I exchange cash before travel instead of using cards?

It depends on the destination, card fees, exchange rate available, how widely cards are accepted locally, and practical safety considerations. Carrying some emergency cash can be useful regardless of which payment method you primarily use. Exchanging large amounts of cash in advance can also carry its own costs and risks. Check your destination’s payment norms and your card terms together before deciding how much cash to carry.

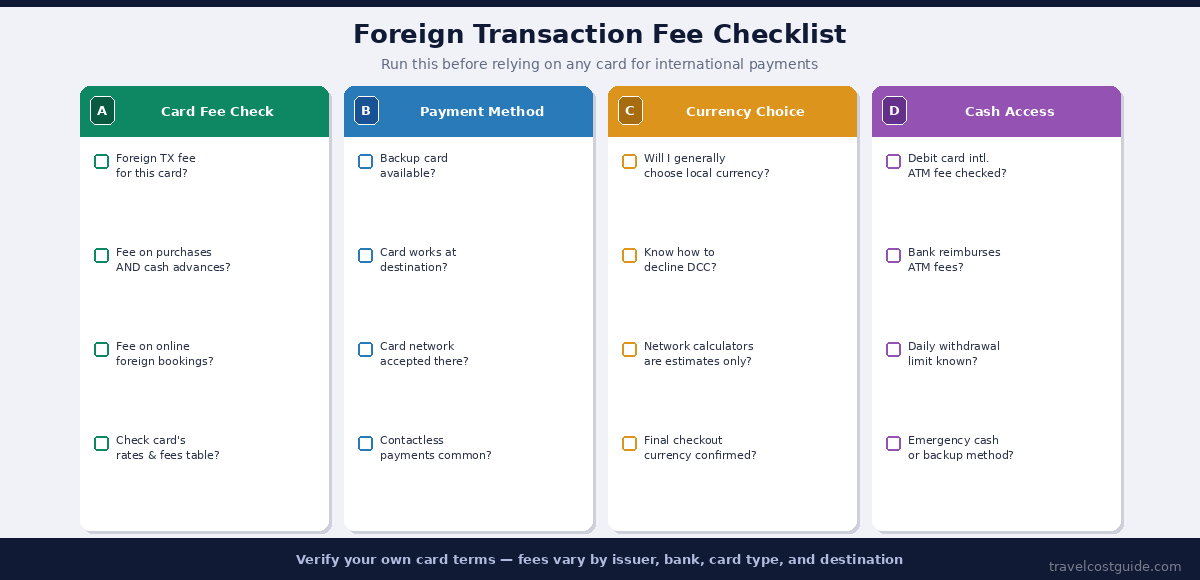

Foreign Transaction Fee Checklist Before You Travel

Before relying on a card abroad, run through this:

Card Fee Check

- Does this card charge a foreign transaction fee?

- Does the fee apply to foreign-currency transactions, foreign merchants, or both?

- Does the fee apply to online bookings made before travel?

- Is there a different rule for cash advances?

Payment Method Check

- Do I have at least one backup card?

- Does my card work reliably at my destination?

- Have I checked whether my card network is widely accepted there?

- Do I know whether contactless payments are standard at my destination?

Currency Choice Check

- Will I generally choose local currency at card terminals when given a choice?

- Do I know how to identify and decline a dynamic currency conversion offer?

- Do I understand that card network calculators show estimates, not guaranteed final amounts?

Cash Access Check

- Does my debit card charge international ATM fees?

- Does my bank reimburse ATM fees?

- Do I know my daily withdrawal limit?

- Do I have emergency cash or a backup payment method if cards are unavailable?

The Bottom Line

Foreign transaction fees are easy to miss because they appear after the purchase — not at the terminal. A traveler may believe they paid one price abroad, then see a different amount on their card statement once conversion, issuer fees, and payment processing rules have been applied.

The approach is straightforward: check your card’s fee terms before travel, use a card whose terms do not charge foreign transaction fees when that makes sense for your situation, choose local currency when offered a conversion choice, and review your statement after the trip to understand the actual cost of each payment.

Foreign transaction fees are one layer of travel payment costs. For a complete picture of all the costs that can affect your trip budget — from flights and accommodation through daily payments — the full breakdown starts with the international trip budget guide.

Read next: What Is Dynamic Currency Conversion — and When to Decline It→