The cash you withdraw abroad may cost more than the amount shown on the ATM screen.

An overseas ATM withdrawal can involve several separate cost layers: your bank’s international ATM fee, the ATM operator’s own fee, a foreign transaction or currency conversion fee applied by your card, an exchange-rate difference, and sometimes a dynamic currency conversion offer at the ATM screen that changes who handles the conversion.

This is the next step after understanding dynamic currency conversion. A traveler can decline DCC correctly at an ATM and still pay an operator fee. A traveler can use a debit card with low bank fees and still pay more if the ATM charges a high access fee. Cash access has its own cost structure, separate from card purchases.

The goal is not to avoid every ATM fee in every country — that is not always realistic. The goal is to understand what can be charged, which fees you can check before travel, and which choices at the ATM screen can prevent unnecessary costs.

Last updated: May 2026. ATM fees, bank policies, card network rules, exchange rates, cash withdrawal limits, and DCC practices can change. Always confirm your own bank, card, and ATM terms before relying on any cash withdrawal strategy abroad.

How this guide was prepared: This guide focuses on practical cash-access checks travelers can make before and during an international trip. It uses official card network guidance, consumer finance resources, and bank-fee disclosure principles as reference points. ATM fees abroad vary by bank, card issuer, ATM operator, country, card network, account type, withdrawal amount, transaction currency, and whether dynamic currency conversion is accepted or declined.

1. What Are ATM Fees Abroad?

ATM fees abroad are the costs that may apply when you use a debit card, ATM card, prepaid card, or credit card to withdraw cash outside your home country. They are not always a single charge — an international cash withdrawal can involve costs from your own bank, the ATM operator, your card’s foreign transaction terms, currency conversion, and — if you use a credit card — cash advance rules.

These costs can stack. Declining one does not automatically remove the others. A traveler who declines DCC can still pay an ATM operator fee and a bank international ATM fee. A traveler who uses a debit card instead of a credit card may still face a foreign transaction fee. Understanding which cost is coming from where is the starting point for managing them.

💡 Practical rule: Treat ATM withdrawals abroad as a separate travel cost category. Do not assume your card’s purchase fee rules are the same as its cash withdrawal rules.

2. The Main ATM Cost Layers

Before using an ATM abroad, separate the possible costs into distinct layers. Not every withdrawal will include every layer, but each one can apply depending on your bank, card, ATM, country, and transaction.

| Cost Layer | Who May Charge It | What to Check |

|---|---|---|

| Your bank’s international ATM fee | Your bank or card issuer | International ATM fee, account fee schedule |

| Out-of-network ATM fee | Your bank, if the ATM is outside its network | Partner network availability, out-of-network fee rules |

| ATM operator fee | The ATM owner or operator | Fee shown on screen before you confirm withdrawal |

| Foreign transaction or currency conversion fee | Your bank or issuer, per card terms | Foreign transaction fee, debit card cross-border fee |

| ATM-side DCC markup | ATM operator or payment processor | Home-currency conversion offer, exchange rate, markup |

| Credit card cash advance costs | Your credit card issuer | Cash advance fee, interest rate, cash advance limit, PIN |

Some banks waive or reimburse certain fees. Some accounts include an ATM fee reimbursement benefit. Some ATMs do not offer DCC. Some destinations rely on cash more than others. But you should understand which layer is which before you withdraw — a withdrawal that looks inexpensive at the ATM screen can become more expensive once your bank’s fees appear on your statement.

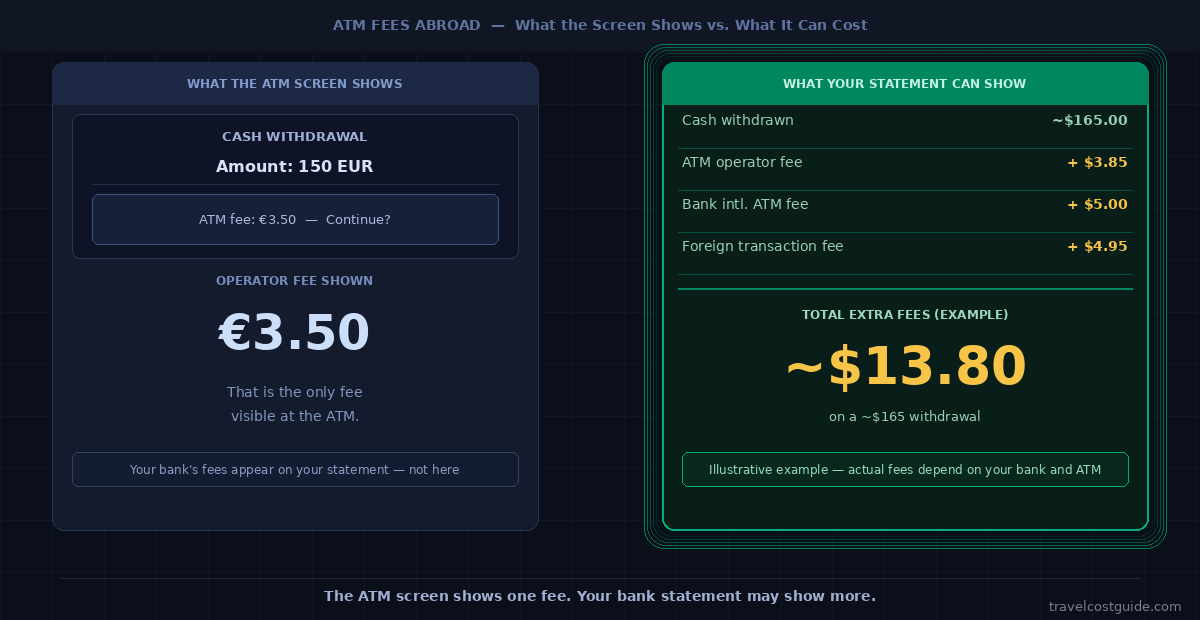

3. ATM Operator Fees: The Charge That Appears on Screen

The ATM operator fee is charged by the owner or operator of the ATM machine you are using. This is typically the fee that appears directly on the ATM screen before you confirm the withdrawal.

The screen may say something like:

- “This ATM charges a withdrawal fee.”

- “A service charge will apply to this transaction.”

- “The ATM operator will charge this fee — your bank may charge a separate fee.”

- “You will be charged [amount]. Do you wish to continue?”

If the ATM discloses an operator fee before you approve the withdrawal, you can usually cancel and look for another ATM. Fee amounts, disclosure formats, and wording vary by country, ATM network, and operator.

Airport ATMs, private convenience-store ATMs, nightlife-area ATMs, and tourist-district ATMs may be physically convenient, but convenience does not always correspond to lower fees. A bank-branch ATM may be cheaper or more transparent in some destinations — but this is not guaranteed and varies by country and network. Always read the screen before confirming.

💡 Practical rule: If an ATM operator fee appears on screen and it seems high, cancel the transaction before confirming. Try a different ATM, a bank-branch ATM, or a different network if available.

4. Your Own Bank’s Fees May Not Appear on the ATM Screen

The ATM operator fee is only one part of the cost. Your own bank or card issuer may also charge an international ATM fee, an out-of-network ATM fee, a debit card foreign transaction fee, or a currency conversion fee — separately from the ATM operator.

These charges may not appear on the ATM screen because they come from your own bank, not from the ATM operator. You may only see them later in your bank account or card statement, sometimes days after the withdrawal.

Before travel, check your bank’s fee schedule for:

- International ATM withdrawal fee

- Out-of-network ATM fee

- Foreign transaction fee on debit card withdrawals

- Currency conversion fee

- ATM fee reimbursement rules and limits

- Daily or per-transaction withdrawal limits

- Card network availability in your destination country

- Partner bank or ATM networks abroad

Some accounts reduce or reimburse certain ATM costs — others charge a fixed fee, a percentage fee, or both. The only reliable answer is your own account disclosure and cardholder agreement. What works for one traveler’s bank may not apply to yours.

5. Dynamic Currency Conversion at ATMs

Dynamic currency conversion can appear at ATMs as well as card terminals. When it does, the ATM offers to convert the withdrawal into your home currency before processing, using a rate set by the ATM operator or payment processor rather than your card network.

You may see prompts such as: “Withdraw in your home currency?” or “Accept guaranteed exchange rate?” or “Continue without conversion?” For a full explanation of how DCC works and what a proper offer should disclose, see the dynamic currency conversion guide.

At ATMs specifically, the important point is this: declining ATM-side currency conversion can help avoid the operator’s conversion rate, but it does not remove other fees. Your bank may still charge an international ATM fee. The ATM operator may still charge its own withdrawal fee. Declining DCC removes one cost layer — it does not make the withdrawal free.

💡 Practical rule: For most travelers, withdrawing in local currency is the cleaner default at an ATM. But you still need to check your bank fee, the ATM operator fee, and your card’s foreign transaction fee separately — those apply regardless of which currency you choose.

6. Debit Card Withdrawals vs. Credit Card Cash Advances

Most travelers use debit cards or ATM cards for cash access abroad. Using a credit card at an ATM is a fundamentally different transaction.

A credit card ATM withdrawal is typically treated as a cash advance, not a normal purchase. Cash advances may involve a cash advance fee charged immediately, interest that begins accruing from the transaction date rather than at the end of a billing cycle, a separate cash advance annual percentage rate that may be higher than the standard purchase rate, a lower cash advance credit limit, and a PIN requirement that varies by card.

The Consumer Financial Protection Bureau notes that withdrawing cash using a credit card is considered a cash advance and can be more expensive than normal card use, and that credit cards may have separate cash advance limits that differ from the standard credit limit.

For most planned cash access, a debit card or ATM card linked to a bank account is one common option — though even then, bank fees, foreign transaction fees, and ATM operator fees still apply. A credit card cash advance is better understood as an emergency option for most travelers, unless you have reviewed the specific terms and find the cost acceptable for your situation.

💡 Practical rule: Before traveling, check whether your credit card allows ATM cash advances, what PIN is required, what fee and interest terms apply, and what the cash advance limit is. Do not discover these details at an overseas ATM.

7. How ATM Fees Can Add Up — and How to Approach Them

The numbers below are only an illustrative example. Your actual costs depend on your bank, ATM operator, card terms, withdrawal amount, currency, country, and whether you accept or decline DCC.

| Cost Item | Example Amount | Notes |

|---|---|---|

| Cash withdrawn | $200 equivalent | Local currency, converted at settlement |

| ATM operator fee | $4.00 | Shown on screen; charged by ATM owner |

| Bank international ATM fee | $5.00 | Charged by your own bank; may not appear on ATM screen |

| Foreign transaction / conversion fee | 3% = $6.00 | Only if your card or bank charges this fee |

| Total extra cost (example) | $15.00 | Before any DCC markup. Illustrative only. |

In this illustrative scenario, a $200 equivalent withdrawal costs $15 in extra fees before any currency conversion markup. Not every traveler will face all three charges — some banks waive fees, some ATMs charge less, and not every card has a foreign transaction fee. But the scenario shows why it is worth checking all layers, not just the one that appears on screen.

One practical consideration is withdrawal size. If fixed fees apply to each withdrawal, withdrawing small amounts repeatedly can make those fixed costs expensive relative to the cash received. Withdrawing a larger amount less often may reduce repeated fee costs — but it also means carrying more cash, which increases the risk of loss or theft. There is no universal best withdrawal amount. The right balance depends on your destination’s cash dependency, how safely you can store cash, your daily spending, and the fees your bank and ATM apply.

Some practical checks that may help reduce avoidable costs:

- Use your bank’s partner network when available. Some banks have international ATM partnerships that waive or reduce certain fees. Confirm the network and participating ATMs before travel.

- Look for bank-branch ATMs where appropriate. In some countries, bank-affiliated ATMs may be more transparent about fees than private or tourist-area ATMs — though this is not universal.

- Decline ATM-side currency conversion in most cases. Withdrawing in local currency generally avoids the ATM-side conversion rate or markup.

- Read the screen before confirming. If the ATM discloses fees or a conversion offer, you can usually cancel before the transaction is processed.

- Carry a backup payment method. Cards can be blocked, lost, or unsupported by a specific ATM or network.

- Know your daily withdrawal limit before you need cash urgently. International limits can differ from domestic ones.

In some destinations, cash remains important for markets, smaller restaurants, rural areas, transport, tips, or small local businesses. In others, card acceptance is widespread and you may only need a small amount of local currency. The right cash strategy depends on where you are going, what you plan to buy, and how widely cards are accepted on your route.

8. Prepaid and Multi-Currency Cards: Check the Full Fee Table

Prepaid travel cards and multi-currency cards can be useful tools for some travelers — for example, when they allow you to hold a destination currency in advance, set a spending limit, or avoid certain conversion steps. But they are not automatically fee-free, and their ATM rules vary significantly by product.

Before relying on a prepaid or multi-currency card for ATM access abroad, check the product’s full fee schedule for:

- ATM withdrawal fee charged by the card issuer

- Free withdrawal allowance per month or per trip, if any

- Fee that applies after the free allowance is used

- Currency conversion fee or spread

- Reload or top-up fee

- Card issuance or delivery fee

- Inactivity fee

- Balance refund or closure fee

- ATM operator fees that may still apply even if the card issuer waives its own fee

A prepaid or multi-currency card with low or no issuer ATM fees can reduce one cost layer, but the ATM operator’s fee still typically applies on top. Compare the card’s full ATM cost structure against your regular bank debit card before deciding which to use — the better option depends on the specific products, destinations, and how much cash you expect to withdraw.

Where to Verify ATM Fees Before Travel

Because ATM fees depend on your specific bank, card, and the ATM you choose, general travel advice cannot replace your own fee disclosures. Verify from primary sources before relying on any cash withdrawal strategy abroad.

- Your bank’s fee schedule: Check international ATM fees, out-of-network ATM fees, foreign transaction fees, currency conversion fees, and reimbursement rules. This is the most important check — different accounts at the same bank can have different rules.

- Your cardholder agreement: Review whether cash withdrawals are treated differently from purchases, and confirm daily limits, PIN requirements, and cash advance terms if relevant.

- Your bank’s ATM network page: Look for partner banks or networks abroad, fee waiver conditions, and supported countries.

- Visa DCC guidance: Review Visa’s Dynamic Currency Conversion guidance to understand what an ATM-side conversion offer should disclose before you accept or decline.

- Mastercard currency converter: Use the Mastercard currency converter as a reference estimate for conversion rates — while noting that issuer fees may apply and Mastercard’s rates may not apply if the ATM operator performs the conversion directly.

- CFPB cash advance guidance: If you are considering using a credit card at an ATM, review the CFPB explanation of credit card cash advances before relying on that option.

- The ATM screen itself: Before confirming any withdrawal, check the disclosed operator fee, the currency choice, the exchange rate if conversion is offered, and any markup. You can usually cancel before committing.

Official tools and fee schedules help you prepare, but the final cost depends on the ATM you use, the card you choose, the amount you withdraw, and how the transaction is processed.

Frequently Asked Questions

Are ATM fees abroad always charged?

No. Some banks and accounts waive or reimburse certain ATM fees, and some ATMs may not charge an operator fee. But many international withdrawals can involve at least one cost layer — your bank’s fee, the ATM operator’s fee, or a foreign transaction fee. Check your own bank terms and read the ATM screen before confirming.

Is the ATM operator fee the same as my bank’s fee?

No. The ATM operator fee is charged by the owner or operator of the ATM machine. Your bank may charge a separate international ATM fee, out-of-network fee, foreign transaction fee, or currency conversion fee on top of that. The ATM operator fee usually appears on screen before you confirm; your bank’s fee may only appear later in your statement.

Should I always decline currency conversion at an ATM?

In many cases, declining ATM-side currency conversion and withdrawing in local currency is the safer default because it avoids the ATM operator’s conversion rate. However, your final cost still depends on your bank fees, card terms, and the exchange rate applied at settlement. Declining DCC does not make the withdrawal free — it removes one cost layer, not all of them.

Can I use a credit card to withdraw cash abroad?

Usually yes, if your card allows cash advances and you have a PIN set. But credit card ATM withdrawals are typically treated as cash advances, not normal purchases — they may involve a cash advance fee, immediate interest, a separate cash advance APR, and a lower cash advance limit. Review your credit card’s cash advance terms before using it for overseas cash access.

Is it better to withdraw one large amount or several small amounts?

It depends on your bank’s fee structure and your destination. If fixed fees apply per withdrawal, fewer withdrawals may reduce total fee costs. But carrying larger amounts of cash increases loss and theft risk, and the right balance also depends on how cash-dependent your destination is. There is no universal best answer — weigh fees against safety and spending needs.

Do prepaid travel cards avoid ATM fees?

Not automatically. Some prepaid or multi-currency cards offer free withdrawal allowances up to a limit, but they may charge after that limit or still pass through ATM operator fees. Check the product’s full fee schedule — including what happens after any free allowance — before relying on it for cash access abroad.

Can an ATM fee be refunded?

Some banks reimburse certain ATM fees, but many do not. Reimbursement rules vary by account type, bank, ATM network, country, and transaction type. Check your bank’s reimbursement policy before travel — and confirm whether the policy covers ATM operator fees, bank fees, or both.

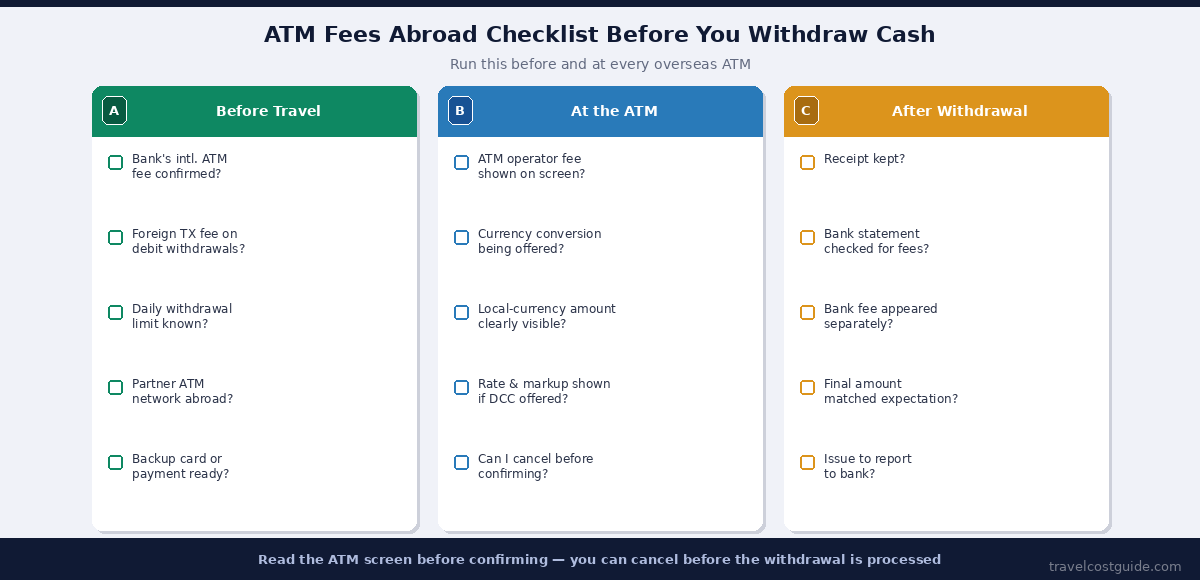

ATM Fees Abroad Checklist Before You Withdraw Cash

Before withdrawing cash overseas, run through this:

Before Travel

- Bank’s international ATM fee confirmed?

- Foreign transaction or conversion fee on debit withdrawals?

- Daily withdrawal limit known?

- Partner ATM network abroad identified?

- Backup card or payment method ready?

At the ATM

- ATM operator fee shown on screen?

- Currency conversion being offered?

- Local-currency withdrawal amount visible?

- Exchange rate and markup shown if conversion offered?

- Can I cancel before confirming if fees look too high?

After Withdrawal

- Receipt kept?

- Bank statement checked for additional fees?

- Final converted amount matched expectation?

The Bottom Line

ATM fees abroad are easy to underestimate because they can come from more than one source. The ATM operator may charge a fee. Your own bank may charge a separate fee. The transaction may also include a foreign transaction or currency conversion fee. The ATM screen may offer dynamic currency conversion, which changes who handles the exchange rate.

A practical approach is to check your bank terms before travel, read the ATM screen before confirming, generally withdraw in local currency to avoid ATM-side conversion, and understand your credit card’s cash advance terms before you need them.

ATM fees are the third layer of international payment costs — alongside foreign transaction fees and dynamic currency conversion. Understanding all three gives you a complete picture of what can affect the cost of paying and accessing cash abroad.

Once your cash-access plan is in place, the next travel cost layer is connectivity: international roaming charges, eSIM plans, pocket WiFi, and local SIM cards can all change the real cost of staying connected during a trip.

Read next: eSIM vs International Roaming: A Real Cost Comparison →