You book the flight. You reserve the hotel. You pay for tours, transfers, and maybe a non-refundable package deal.

Then one question appears before checkout:

Do you want to add travel insurance?

For many travelers, this is where the confusion starts. The price may look small next to the full trip cost — but it is not always clear what that price actually buys. Is it medical protection? Trip cancellation? Lost baggage? Emergency evacuation? A partial refund if your plans change?

The answer depends largely on the policy.

This guide explains travel insurance costs from a practical travel budgeting perspective. It does not recommend a specific insurance company, policy, credit card, broker, or travel product. Instead, it explains the cost layers travelers should compare before buying — including cancellation, interruption, medical coverage, evacuation, baggage, delays, deductibles, exclusions, and claim documentation.

Important note: Travel insurance benefits depend on the exact policy wording, destination, trip dates, purchase timing, exclusions, limits, deductibles, and required documentation. This article is general travel cost information — not legal, medical, or insurance advice. Read the full policy documents and confirm current terms with the insurer or a licensed professional before buying.

How this guide was prepared: This guide was developed using publicly available information from government travel agencies, national insurance regulators, and consumer health authorities. No insurance company, broker, credit card provider, or travel product has sponsored or influenced this content. Examples used are illustrative only and do not reflect the terms of any specific policy.

Travel insurance is not one single cost. Policy wording, covered reasons, exclusions, deductibles, documents, and credit card benefits can all affect the practical value.

Travel Insurance Is Not One Single Cost

Travel insurance often appears as a single line item at checkout — one price, one purchase. But that price may reflect several different types of potential protection bundled together, or it may cover only one narrow area, depending on the product.

A policy may include trip cancellation, trip interruption, emergency medical coverage, medical evacuation, baggage delay, baggage loss, travel delay, missed connection, rental car coverage, or emergency assistance services. Some policies bundle several of these together. Others focus mainly on medical coverage or trip cancellation. Some credit cards also include limited travel protections when you pay for a trip with that card — but card benefit limits and conditions can be narrower than a standalone policy.

This is why comparing travel insurance by price alone can be misleading. A lower-priced policy may carry lower benefit limits, higher deductibles, narrower covered reasons, or more exclusions. A higher-priced policy may include benefits you do not need for a simple trip. The better question is not just: How much does travel insurance cost? The better question is: What risks are you paying to reduce, and what situations are actually covered under this policy?

Travel insurance is one part of the total cost of planning an international trip. If you are still working through your full budget, The Real Cost of an International Trip — Before You Book explains how flights, hotels, payment fees, mobile data, local transport, and booking terms can all affect your final cost before departure.

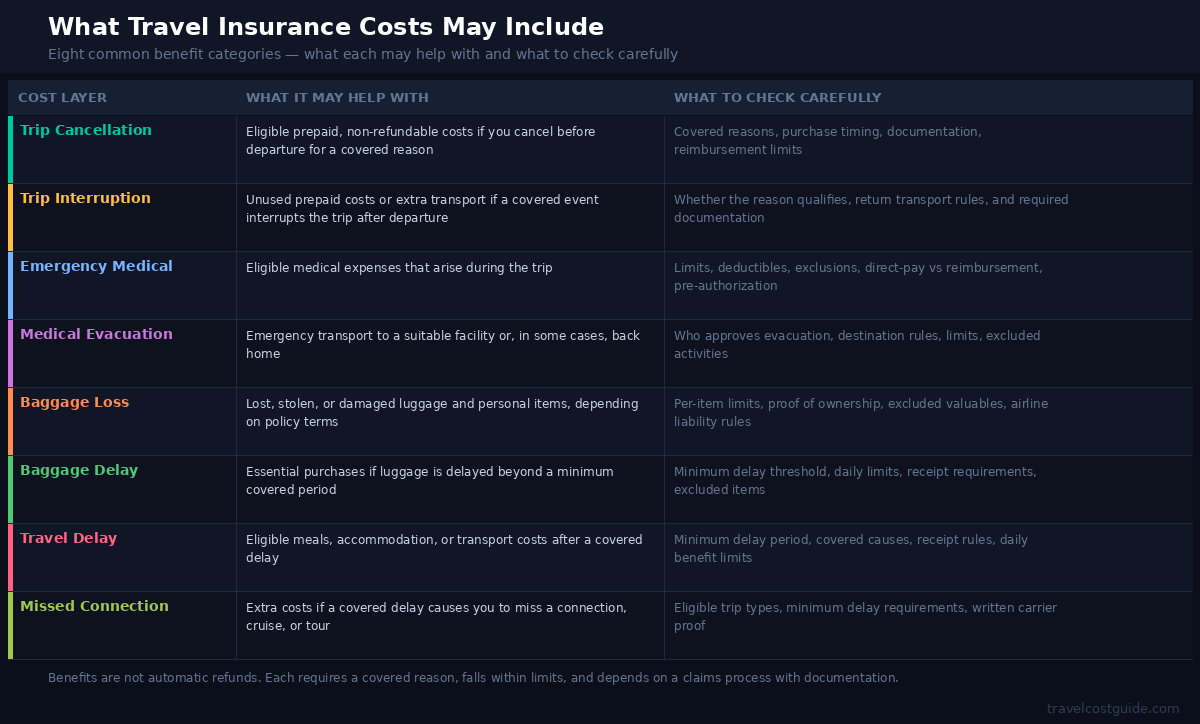

What Travel Insurance Costs May Include

A travel insurance premium may reflect several benefit categories, but each one depends on covered reasons, limits, exclusions, deductibles, and documentation.

A travel insurance premium may reflect several benefit categories. Not every policy includes every category, and the names and terms can vary by provider, country of purchase, and product type. Understanding these common categories before buying can help you compare policies more accurately.

Cost Layer

What It May Help With

What to Check Carefully

Trip cancellation

Eligible prepaid, non-refundable costs if you cancel before departure for a covered reason

Covered reasons, purchase timing, required documentation, and reimbursement limits

Trip interruption

Unused prepaid costs or extra transport if a covered event interrupts the trip after departure

Whether the reason qualifies, how return transport is handled, and documentation needed

Emergency medical

Eligible medical expenses that arise during the trip

Coverage limits, deductibles, exclusions, direct-pay vs reimbursement rules, and pre-authorization requirements

Medical evacuation

Emergency transportation to a suitable medical facility or, in some cases, back home

Who decides evacuation is necessary, destination rules, benefit limits, and excluded activities

Baggage loss or damage

Lost, stolen, or damaged luggage and personal items, depending on policy terms

Per-item limits, proof of ownership requirements, excluded valuables, and airline liability rules

Baggage delay

Essential purchases if luggage is delayed beyond a minimum covered period

Minimum delay threshold, daily limits, receipt requirements, and excluded items

Travel delay

Eligible meals, accommodation, or transport costs after a covered delay

Extra costs if a covered delay causes you to miss a connection, cruise, or tour

Eligible trip types, minimum delay requirements, and written proof from the carrier

These benefits are not automatic refunds for any travel inconvenience. Each benefit typically requires a covered reason, falls within defined limits, may have deductibles and exclusions, and depends on a claims process that requires documentation. That is why the policy wording matters more than the marketing headline.

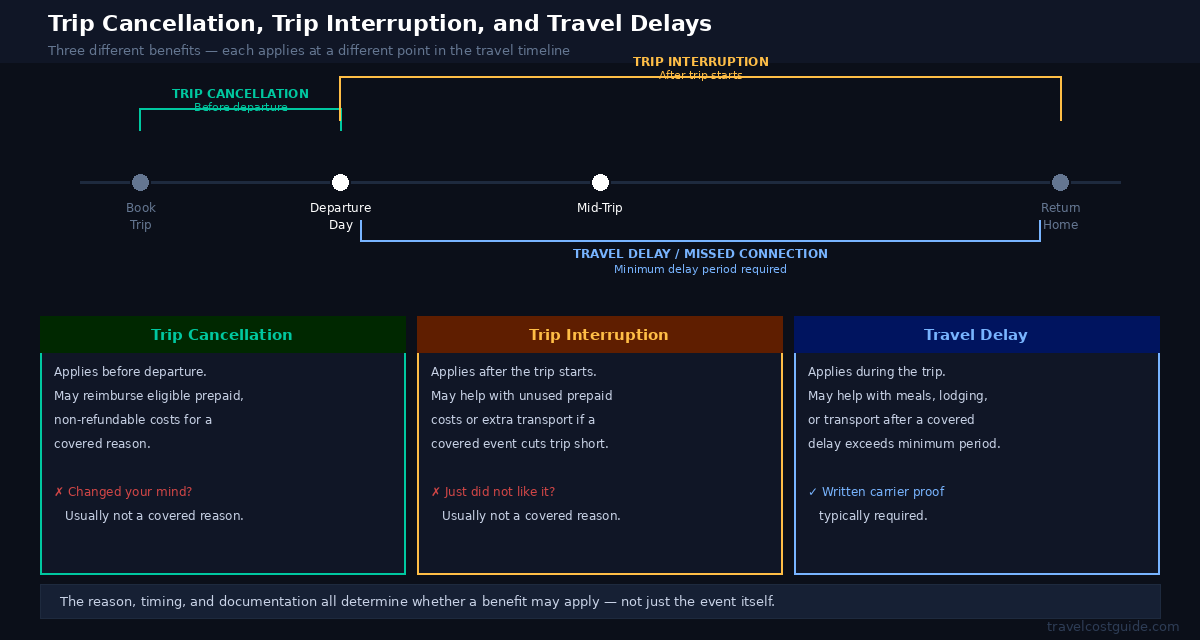

Trip Cancellation, Trip Interruption, and Travel Delays

Trip cancellation generally applies before departure, while trip interruption and travel delay may apply after the trip has started, depending on policy terms.

Three of the most commonly misunderstood benefits in travel insurance are trip cancellation, trip interruption, and travel delay. Each applies at a different point in the travel timeline — and each has its own covered reasons, limits, and documentation requirements.

Trip Cancellation

Trip cancellation generally applies before the trip starts. It may help reimburse eligible prepaid and non-refundable costs if you cancel for a covered reason. Common examples may include serious illness, injury, certain family emergencies, or other events listed in the policy. Canceling because you changed your mind, found a cheaper option, or no longer want to travel is typically different from canceling for a covered reason. The exact list of covered reasons varies by policy.

Trip Interruption

Trip interruption generally applies after the trip has already started. It may help with unused prepaid travel costs or additional transportation if a covered event forces you to cut the trip short or change plans mid-trip. The same principle applies: the reason matters, the timing matters, and the documentation matters.

Travelers with expensive flights, cruises, tours, or prepaid hotel packages should read both sections carefully. If you booked a non-refundable hotel, also review the hotel’s own cancellation terms before assuming insurance will cover the full amount. For more on how hotel cancellation rules can affect your costs, read Hotel Fees Guide: What Travelers Should Check Before Booking.

Travel Delay and Missed Connections

Travel delay coverage may help with extra expenses such as meals, accommodation, or local transport when a covered delay exceeds the policy’s minimum delay period. Missed connection coverage may help if a covered delay causes you to miss a cruise, tour, or connecting flight, depending on policy terms.

These benefits are especially relevant for travelers booking tight connections, separate tickets, cruises, or non-refundable accommodations after arrival. Most policies require written proof from the airline or carrier showing the cause and duration of the delay. Flight-related costs can also appear before insurance is involved — seat selection fees, baggage charges, schedule changes, and separate-ticket connection risks all affect the real cost of flying. For a broader breakdown, read Hidden Flight Costs: What Travelers Should Check Before Booking.

Emergency Medical Coverage Abroad

Emergency medical coverage is one of the most consequential parts of many travel insurance decisions, especially for international trips. Your regular health insurance may not cover medical care abroad, or it may apply only in limited circumstances. Some travelers may also face upfront payment requirements at clinics or hospitals overseas before any insurance reimbursement is possible.

A travel medical benefit may help with eligible emergency treatment costs during the trip — which can include doctor visits, hospital care, medication, or emergency treatment related to illness or injury. However, coverage limits, deductibles, excluded conditions, provider network rules, and pre-authorization requirements can vary widely between policies.

Before buying, check:

whether the policy covers your specific destination;

whether emergency and routine care are treated differently;

whether pre-authorization is required before receiving certain care;

whether the insurer pays the provider directly or reimburses you after the trip;

whether pre-existing medical conditions are excluded or require a separate waiver;

whether alcohol, risky activities, or self-inflicted injuries are excluded;

whether the policy includes a 24/7 emergency assistance contact number.

A high benefit limit on paper may still leave gaps if the deductible is high, the activity is excluded, the condition is pre-existing, or the required claim documents are difficult to provide after the trip.

Medical Evacuation, Repatriation, and Remote Travel

Medical evacuation coverage is distinct from standard emergency medical coverage. It may help cover emergency transportation to an appropriate medical facility or, in some situations, transportation back to your home country. Repatriation may refer to returning remains home in the event of death abroad, depending on the specific policy wording.

This benefit can be especially relevant for remote destinations, cruise travel, adventure trips, areas with limited medical infrastructure, or situations where the nearest suitable hospital may be far from where the emergency occurs. However, the policy typically defines when evacuation is considered medically necessary, who is authorized to approve it, and where the traveler can be transported.

Travelers should not assume they can choose any hospital or request evacuation to a preferred location simply because they prefer it. Most policies require coordination through the insurer’s emergency assistance team. Some benefits may not apply if the injury or illness occurs during an excluded activity — such as extreme sports or other activities specifically excluded from the policy.

Before buying, check:

who determines whether evacuation is medically necessary;

whether evacuation must be pre-approved by the insurer;

whether the benefit transports you to the nearest suitable facility or to your home country;

whether adventure activities, mountaineering, diving, or remote expeditions are excluded;

whether cruise, island, or wilderness travel has special conditions or exclusions;

whether the emergency assistance number works internationally, including in your specific destination.

Baggage Loss, Delay, and Personal Items

Baggage coverage can be useful, but it is one of the most frequently misunderstood areas of travel insurance. A policy may include benefits for lost, stolen, damaged, or delayed baggage — but the amount a traveler may receive depends on item limits, category sub-limits, receipts, proof of ownership, airline documentation, and whether the item falls into an excluded category.

Expensive electronics, cameras, jewelry, sports equipment, cash, passports, or business equipment often have lower sub-limits or are explicitly excluded. A baggage delay benefit may only apply after a minimum delay period has passed, and it may only reimburse reasonable, documented essential purchases.

Airlines also have their own baggage liability rules, which may apply before travel insurance does. Most travel insurance policies require you to file a claim with the airline first, obtain a written property irregularity report, or provide written confirmation of the delay or loss before a claim can be processed.

Before relying on baggage coverage, check:

the total baggage benefit limit;

per-item and category sub-limits;

whether electronics, jewelry, cash, or documents are excluded or have separate limits;

the minimum delay time before baggage delay benefits apply;

what receipts or proof of ownership are required;

whether an airline or carrier report is required before the insurance claim can be filed.

Pre-Existing Conditions, Exclusions, and Activity Limits

Two of the most important sections to review before buying travel insurance are pre-existing medical conditions and activity exclusions. Both can affect what is — and is not — covered under a policy.

Pre-Existing Medical Conditions

A medical condition you had before purchasing the policy may be excluded from coverage unless the policy includes a waiver and you meet specific eligibility requirements. Those requirements can vary: some policies may require you to purchase coverage within a certain number of days after your first trip deposit. Others may require you to insure the full prepaid trip cost. Some may require that you were medically stable and able to travel when the policy was purchased. Others may not offer a waiver at all.

This is not a section to skim. If you, a traveling companion, or a non-traveling family member has an ongoing medical condition, recent treatment history, medication changes, pregnancy-related considerations, or any health situation that could affect travel plans, review the policy wording carefully and ask the insurer directly before purchasing.

Questions to ask include:

How does this policy define a pre-existing condition?

What look-back period applies?

Is a waiver available, and what are the eligibility requirements?

When must the policy be purchased to qualify for the waiver?

Does the waiver also apply to non-traveling family members?

What medical records may be required if a claim is filed?

Adventure Activities, Alcohol, and Other Exclusions

Most travel insurance policies include a list of exclusions — situations where the policy may not pay, even when a genuine loss or emergency occurs. Common exclusions may involve high-risk activities, professional or competitive sports, certain adventure activities, alcohol or drug-related incidents, reckless behavior, travel against official government advisories, illegal acts, and known events or conditions that existed before the policy was purchased.

Travelers planning activities such as skiing, scuba diving, motorbike riding, trekking, mountaineering, surfing, skydiving, or remote expeditions should check the activity list in the policy — not just the general category description. Some standard policies exclude these activities entirely. Others may cover them only under specific conditions, at certain altitudes or depths, with required licenses or equipment, or through an add-on that must be purchased separately.

Before buying, check whether your planned activities are specifically covered, including altitude limits, depth limits, helmet or equipment requirements, alcohol exclusion language, and whether a separate rider or specialty policy may be needed.

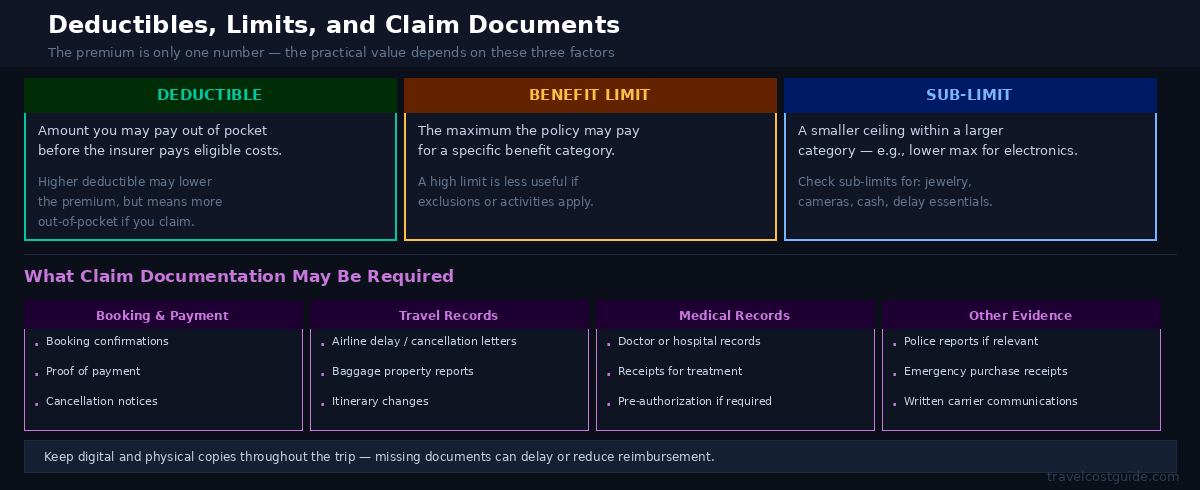

Deductibles, Limits, and Claim Documents

The practical value of a travel insurance policy depends on deductibles, benefit limits, sub-limits, exclusions, and the documents required for a claim.

The premium is only one number. The practical value of a travel insurance policy depends on the deductible, benefit limits, sub-limits, exclusions, and the claims process you would need to follow if something went wrong.

A deductible is the amount you may be required to pay out of pocket before the insurer pays eligible costs. A benefit limit is the maximum amount the policy may pay for a specific category. A sub-limit is a smaller ceiling within a larger benefit category — for example, a lower maximum specifically for electronics, jewelry, or baggage delay essentials.

Claims documentation is equally important. If you cannot provide the required documents, reimbursement may be delayed, reduced, or denied. Before travel, understand what documentation a claim would require, and during the trip, keep everything that might be relevant: receipts, booking confirmations, medical records, airline delay or cancellation letters, police reports, property irregularity reports, proof of payment, and written communication from airlines, hotels, doctors, or tour operators.

Before buying, review:

the deductible amount for medical and non-medical claims;

the maximum benefit limit for each coverage category;

sub-limits for baggage, valuables, electronics, or delay-related expenses;

the claim filing deadline after an incident;

whether original receipts are required or whether digital copies are accepted;

whether written proof from an airline, hotel, doctor, or police is required;

whether the insurer requires you to contact emergency assistance before receiving treatment or arranging evacuation.

Credit Card Travel Protection vs Standalone Policy

Some credit cards include travel protection benefits when you pay for eligible trip costs with the card. These benefits can provide useful coverage for certain travelers in certain situations — but they should not automatically be assumed to replace a standalone travel insurance policy.

Credit card travel protection may have lower benefit limits, fewer covered reasons, shorter eligible trip lengths, or no emergency medical coverage at all. Some cards focus primarily on trip delay, baggage delay, or rental car collision damage. Others offer broader benefits that may include trip cancellation or interruption. Eligibility often depends on paying for the trip with that specific card, using rewards points through the card’s travel program, or meeting other booking conditions defined in the cardholder benefit guide.

Before relying on credit card benefits, check:

which specific benefits are included under your card;

whether emergency medical coverage is included or excluded;

whether medical evacuation is included;

whether the full trip cost must be paid with the card to activate benefits;

whether award tickets or partially paid bookings qualify;

who is covered: cardholder only, spouse, dependent children, or travel companions;

any trip length limits, destination exclusions, or benefit expiration rules;

the benefit administrator’s contact information and claims process.

A standalone policy may offer more customizable coverage for medical, cancellation, evacuation, or family situations. A credit card benefit may be sufficient for some lower-risk, lower-cost trips. The right comparison depends on your specific trip cost, destination, health needs, family situation, and what card benefits are actually available to you.

Travel insurance is one layer of cost protection. It works best when the other layers — refundable bookings, payment card protections, and accessible mobile connectivity for emergencies — are also reviewed before departure. For phone access and emergency communication planning, read eSIM vs International Roaming: A Real Cost Comparison.

💡 When insurance may be less useful: Travel insurance may offer limited value when most bookings are fully refundable, the trip cost is low, your existing health insurance clearly covers the destination and trip type, your credit card already provides the protection you need, or the activities you plan to do are excluded from the policy. The value of a policy depends on what you are trying to protect — compare it against your non-refundable costs, destination risks, and actual policy terms.

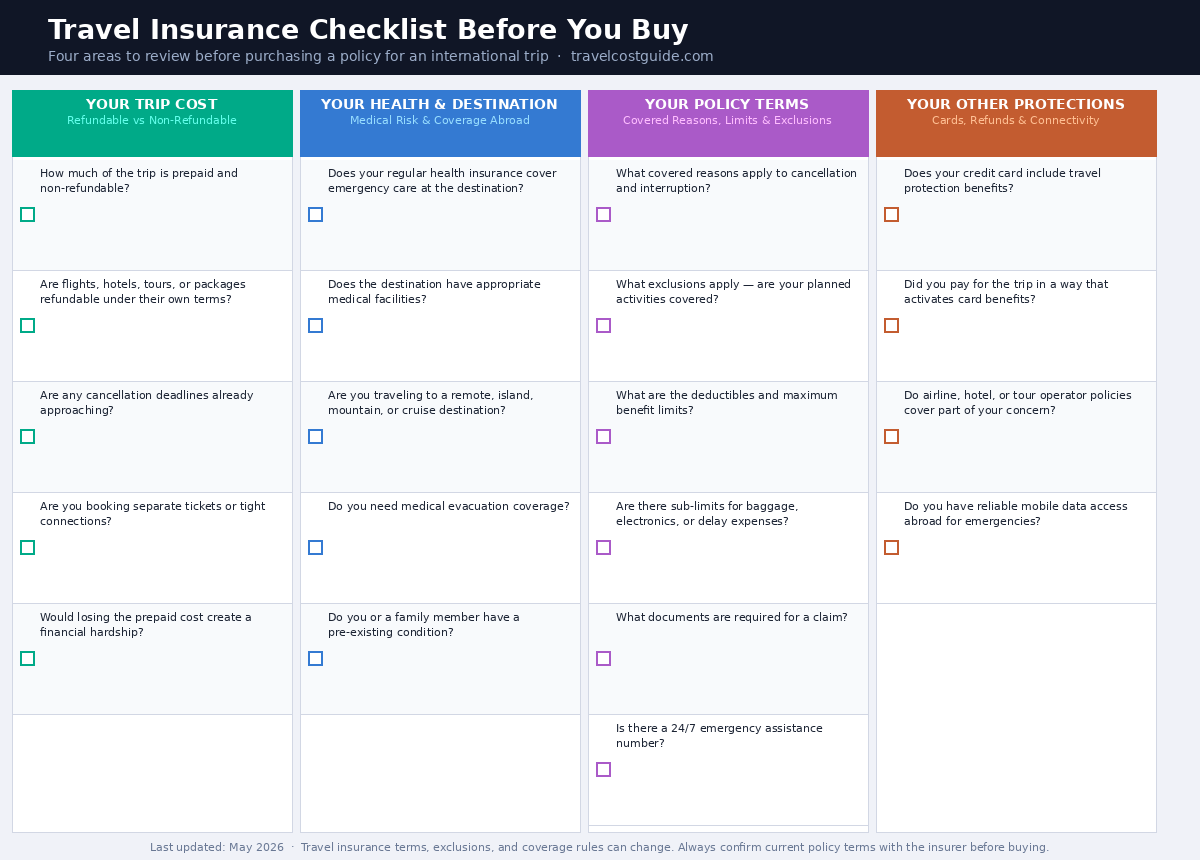

Travel Insurance Checklist Before You Buy

Before buying travel insurance, compare your non-refundable trip cost, destination risks, health coverage, exclusions, limits, and required claim documents.

Use this checklist before purchasing travel insurance for an international trip.

Your Trip Cost

☐ How much of the trip is prepaid and non-refundable?

☐ Are flights, hotels, tours, cruises, or packages refundable under their own terms?

☐ Are any cancellation deadlines already approaching?

☐ Are you booking separate tickets or tight connections?

☐ Would losing the prepaid trip cost create a significant financial hardship?

Your Health and Destination

☐ Does your regular health insurance cover emergency care at your destination?

☐ Does the destination have medical facilities appropriate for your needs?

☐ Are you traveling to a remote area, island, cruise ship route, mountain region, or rural destination?

☐ Do you need medical evacuation coverage given the destination and activities planned?

☐ Do you or a traveling family member have a pre-existing condition that could affect coverage?

Your Policy Terms

☐ What covered reasons apply to cancellation and interruption benefits?

☐ What exclusions apply — and are your planned activities covered?

☐ What are the deductibles and maximum benefit limits for each category?

☐ Are there sub-limits for baggage, electronics, jewelry, or delay-related expenses?

☐ What documents are required for a claim?

☐ Is there a 24/7 emergency assistance number that works at your destination?

Your Other Protections

☐ Does your credit card include travel protection, and which benefits does it cover?

☐ Did you pay for the trip in a way that activates those card benefits?

☐ Do airline, hotel, or tour operator refund policies already address part of your concern?

☐ Do you have reliable mobile data access abroad to contact insurers, airlines, and hospitals in an emergency?

Mobile access can be important during travel emergencies and insurance claims. If you have not yet planned your phone connectivity abroad, read eSIM vs International Roaming: A Real Cost Comparison before departure.

Frequently Asked Questions

How much does travel insurance usually cost?

Travel insurance cost depends on many variables: the total trip cost, traveler age, destination, trip length, type of coverage, benefit limits, deductibles, add-ons, and when the policy is purchased. A policy for a short, lower-cost trip may cost much less than one for an expensive cruise, remote destination, or extended international trip. Instead of comparing only the premium, compare what the policy may cover, what it excludes, and whether the benefit limits match your actual trip.

Does travel insurance cover trip cancellation for any reason?

Standard trip cancellation coverage applies only to covered reasons listed in the policy. Canceling because you changed your mind, found a better deal, or simply decided not to travel may not qualify. Some policies offer a separate “cancel for any reason” option, but availability, purchase timing requirements, eligible reimbursement percentages, and conditions vary. Read the policy wording before assuming this benefit applies.

Is travel medical insurance the same as trip cancellation insurance?

No. Travel medical insurance focuses on eligible medical expenses that occur during the trip. Trip cancellation insurance focuses on eligible prepaid, non-refundable trip costs if you cancel before departure for a covered reason. Some comprehensive policies may include both types of coverage, but the two benefits have different rules, limits, and claim requirements.

Does travel insurance cover pre-existing medical conditions?

It depends on the policy. Many policies exclude pre-existing conditions unless a waiver applies and specific requirements are met — such as purchasing the policy within a defined number of days after your first trip payment, insuring the full prepaid trip cost, or being medically able to travel at the time of purchase. Travelers with health conditions should review this section carefully and ask the insurer directly before buying.

Will travel insurance pay the hospital directly?

Some policies may arrange direct payment with certain hospitals or providers through their emergency assistance network. Others may require you to pay out of pocket first and file a claim for reimbursement later. Rules vary by insurer and situation. Before departure, check whether the policy has a 24/7 emergency assistance number, whether pre-authorization is required, and how medical payment or reimbursement is handled at your destination.

Is credit card travel insurance enough?

It may be sufficient for some trips, depending on the card benefits and your specific needs. Credit card travel protection may have lower benefit limits, fewer covered reasons, trip length restrictions, or no emergency medical coverage. Review your card’s benefits guide and compare it with a standalone policy if medical coverage, evacuation, trip cancellation, or family member coverage is important for your trip.

Should I buy travel insurance for a refundable trip?

If most of your trip is refundable and your existing health coverage clearly applies at the destination, the practical value of a standalone travel insurance policy may be more limited. However, medical evacuation coverage, emergency medical benefits, travel delay, or emergency assistance services may still be relevant depending on the destination and trip type. Compare the premium against the actual non-refundable costs and destination risks before deciding.

What documents should I keep for a travel insurance claim?

Keep booking confirmations, receipts, proof of payment, cancellation notices, airline delay or cancellation letters, baggage reports, medical records, police reports where relevant, and written communication from airlines, hotels, doctors, tour operators, or other service providers. Many travel insurance claims depend heavily on documentation — keep both digital and physical copies throughout the trip when possible.

Bottom Line

Travel insurance costs are not just about the premium. You are paying for a set of potential benefits — each with its own covered reasons, limits, deductibles, exclusions, and documentation requirements.

A policy may help with prepaid trip costs, emergency medical care, evacuation, baggage problems, travel delays, or trip interruption after departure. But it may not cover every reason, every activity, every medical condition, or every loss.

The most practical way to evaluate travel insurance is to start with your specific trip: how much is non-refundable, where you are going, what medical risks exist at the destination, whether your regular health insurance applies abroad, whether evacuation coverage is relevant, and whether you could provide the documentation a claim would require.

The cheapest policy is not always the most useful one. A better policy is the one that matches the real risks of your trip, explains its limits clearly, and gives you a claims process you can actually follow.

Where to Verify

Before buying travel insurance, check official sources and read the current policy documents. These references explain common coverage categories, medical travel risks, and consumer protection considerations:

Travel insurance is one part of the larger international travel cost picture. These guides cover other cost layers to review before booking and departure:

Last updated: May 2026. Travel insurance products, exclusions, medical coverage rules, cancellation benefits, and claim requirements can change. Confirm current terms directly with the insurer, policy documents, and relevant official sources before buying.